On 7 September Governor Phillip Lowe, released a statement on behalf of the Reserve Bank detailing the latest monetary policy decision of the board.

“At its meeting today, the Board decided to:

- maintain the cash rate target at 10 basis points and the interest rate on Exchange Settlement balances of zero per cent

- maintain the target of 10 basis points for the April 2024 Australian Government bond

- purchase government securities at the rate of $4 billion a week and to continue the purchases at this rate until at least mid February 2022.

Prior to the Delta outbreak the Australian economy had considerable momentum. GDP increased by 0.7 per cent in the June quarter and by nearly 10 per cent over the year. Business investment was picking up and the labour market had strengthened. The unemployment rate had fallen below 5 per cent and job vacancies were at a high level,” according to Governor Lowe.

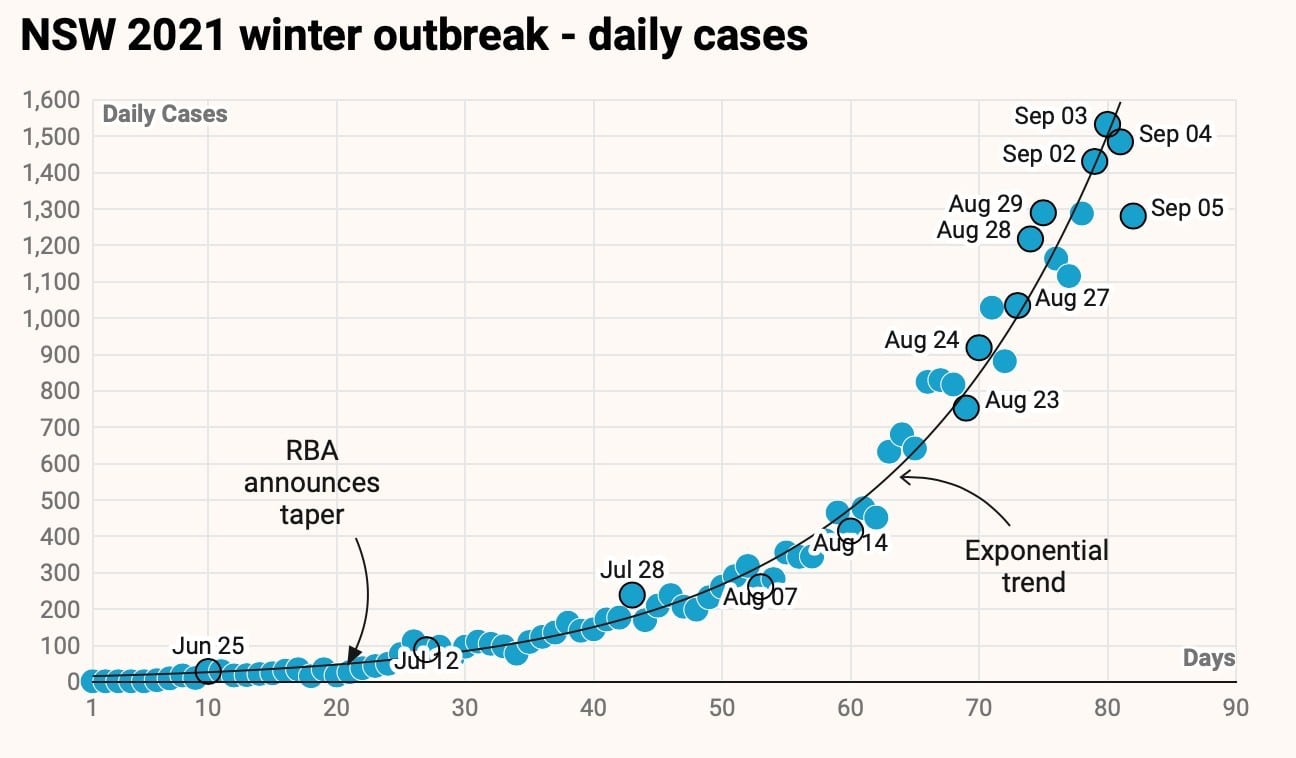

The decision to maintain the cash rate at 0.1% was also accompanied by a decision to reduce weekly bond purchases from $5 billion to $4 billion per week. The Reserve Bank declared their intention to cut back on weekly bond purchases in July and possibly after mid-November since the Australian economy appeared to be recovering nicely. A week after this announcement, however, there was a surge in NSW’s daily case rate and most of the state remains under restrictions or lockdown at the time of writing.

The RBA did contemplate suspending the plan to reduce weekly bond purchases in August – as the daily cases continued to climb – but has ultimately decided to press on with the $1billion cut. However, it committed to maintaining this bond purchase rate until mid-February rather than cutting it again in December.

Source: Greg Jericho via the Guardian

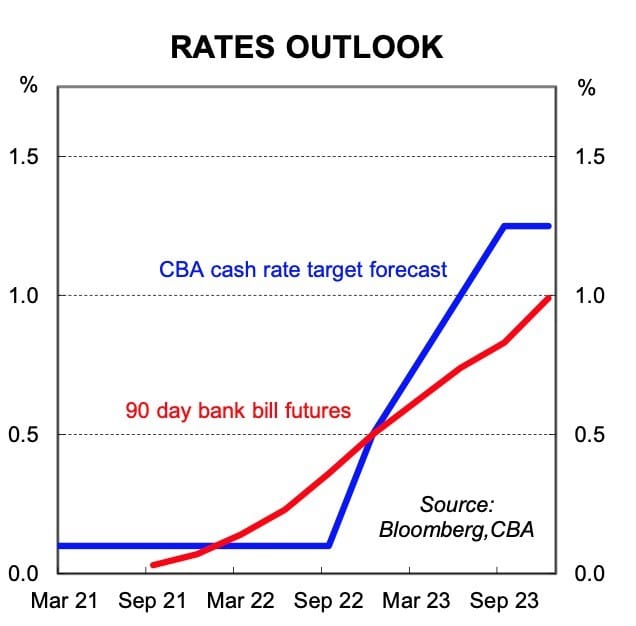

Before to the Delta outbreak in June, the economic recovery was in an upswing and the unemployment rate dropped significantly to 5.1% – down from 5.5% – in May. This lead Bill Evans – the Chief Economist of Westpac – to forecast that Government intervention policies could consequently be eased and that interest rate increases might occur in the first quarter of 2023, rather than the third or fourth quarter. However, the Commonwealth Bank of Australia (CBA) felt that interest rates would rise even sooner than what Westpac forecasted — starting in November 2022.

During the ongoing lockdowns; economic conditions have become much tougher on micro, small and medium business owners. Non- essential enterprises were forced to temporarily close and government support packages were delayed or fell short of business overheads. ANZ-Roy Morgan recorded a 1.8 point drop in consumer confidence in the first week of September.

Three of the four big banks – CBA, ANZ and Westpac – were anticipating the Reserve bank would keep the bond purchasing figures unchanged. But, Governor Lowe referred to the Delta drop as merely a setback to economic expansion and forecast that our economy should be back on track by late 2022.

“This setback to the economic expansion is expected to be only temporary. The Delta outbreak is expected to delay, but not derail, the recovery. As vaccination rates increase further and restrictions are eased, the economy should bounce back. There is, however, uncertainty about the timing and pace of this bounce-back and it is likely to be slower than that earlier in the year… in our central scenario, the economy will be growing again in the December quarter and is expected to be back around its pre-Delta path in the second half of next year”, the Governor wrote.

It comes as no surprise that homeowners and investors are watching these fluctuating forecasts and interest rates closely. Some mortgage holders are even electing to safeguard their position by fixing part or all of their mortgage. Over 50% of those polled in recent research – by Finder – worry about increasing interest rates and, 15% of those with a mortgage are not confident in their ability to meet higher repayments. Australian Bureau of Statistics data (ABS) indicates that fixed interest loans have doubled from 20% to 40%, “The value of refinancing between lenders was 60 per cent higher in July 2021 compared to a year ago,” said Katherine Keenan of the ABS.

Governor Lowe and the Reserve Bank board maintain an optimistic outlook on the ability of the Australian economy to bounce back yet again. The decision to hold interest rates at 0.1% and to delay further reviews of the bond purchasing rate until 2022, suggests that this is not blind optimism, but rather a forecast that is supported by the modelling. If the road map to recovery does go as planned, it is likely that the banks’ forecast of economic growth returning in the December quarter will eventuate.

This is arguably the best time to review your mortgage and the financial structure of your property portfolio. Are you able to weather any potential interest rate rises or is there an untapped opportunity to get a better rate on your mortgage? Contact Trilogy today for a free 30-minute finance strategy session to find out.

About the Author

Since 2008, David Thomas has built a business aimed at servicing the needs of property investors. Now recognised as one of the top 10 independent mortgage brokerages in the country, David and his team have settled almost 2 billion dollars worth of residential and investment loans over the last decade.

Known for his straightforward, accessible style, David believes by educating people about their mortgages; they fare better in the market. By sharing his expertise openly, some of the people he educates will likely become his clients. It's a win-win approach.

David Thomas is a credit representative (Representative Number 506153) of BLSSA Pty Ltd, ACN 117 651 760 (Australian Credit Licence 391237).