Not since the decade that saw rock and roll truly emerge as an iconic aspect of American culture have variable interest rates been trending as low as they are right now.

Despite the far more focused regulatory eye APRA is directing at property investment lending activity, many banks are offering enticingly good variable deals at less than 5 per cent – the lowest since the 1950s. With some of the best fixed rates for one to two years under 4 per cent.

Credit is almost going begging. And if the Reserve Bank does indeed maintain rates at their current low level for the remainder of the year, as many anticipate, you can guarantee more punters will jump on the property bandwagon.

Why wouldn’t you? Cheap credit, buoyant inner city markets that consistently prove to deliver with strong growth and yields, and a collective shift in how younger generations perceive property ownership that will invariably see real estate become more of a commodity as demand continues to grow…

Seems to be the perfect property investment storm. But is it too perfect?

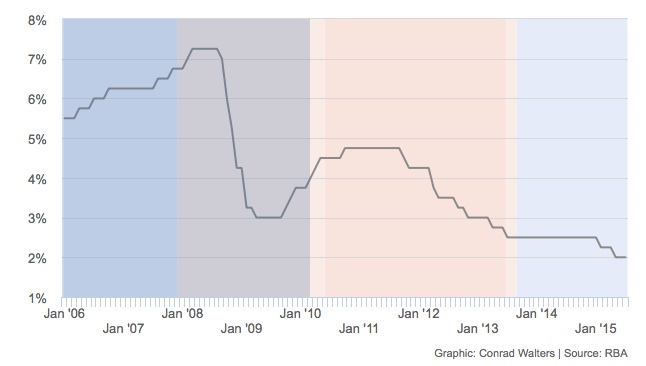

Interest rate movements 2006 to 2015

The calm before…

Some would argue that we’re currently in the eye of the storm, and as with any market in a state of volatile flux (such as a housing bubble about to implode), there could be a few dark clouds on the horizon.

If history teaches us one thing about any type of commodity – housing being no exception – it’s that there’ll always be swings in fortunes. They could go in favour of the investor, or against, at any given time.

Those who can ride out the storm…bunkering down when things get a little too full on, and sustaining their investment portfolio with airtight asset selection, structuring, finance and management…will soon step back into the sunlight, having survived the chaos.

Then there are those who ‘never saw it coming’. The ones who get caught ‘out at sea’ in a market monsoon, and carried away on a tide of transition that may or may not see them come out with their portfolio intact.

At this present time, low interest rates and constant reports about ‘unprecedented’ escalations in housing values are encouraging a lot of buyers into real estate.

But neither low interest rates, nor a moment in time when the markets happen to be peaking, mean that the inherent risk associated with real estate (as with any type of investment) is eliminated altogether.

In fact, it could be said that the opposite is true…with many diving in too enthusiastically before checking the forecast, consulting a compass and assessing the potential pitfalls.

Now more than ever, you need to remember that low rates DO NOT equal low risk! Here are five key risks you need to weigh up at this time…

-

Paying too much

Competition is fierce, but that doesn’t mean you should join those who end up in frenzied bidding wars, just to say you had a win!

A number of industry experts suggest that in some highly sought after suburbs, where auctions are the standard way of moving homes, stock can currently sell for as much as 20 to 30 per cent over market value at the fall of the hammer.

When you consider many of these are high-end postcodes to begin with, you can see the very obvious issues here.

For starters, if (and when) the market cools, property owners could find themselves in a negative equity position – owing more on their mortgage than what their home is worth.

In other words, the risk is that you end up with a liability rather than an asset and moreover, a liability that you’ll either have to sell at a loss, or retain in the hopes of regaining some of that lost capital ground.

Paying too much is particularly problematic for investors making off the plan acquisitions, who could find that when it comes to finalizing your loan contract, the lender decides the security (ie. new apartment) isn’t actually worth enough to cover the amount you need to borrow.

-

Failing to research

When buyers start to feel a sense of urgency about getting into the market before there’s nothing left (and what is available is completely unaffordable), they tend to make snap decisions.

I guarantee there’ll be many a new investor who neglects to do the appropriate research and ends up with a dud, because not all properties are investment grade.

If you’re investing based on what everyone else is doing rather than facts and figures, then the wealth you hope to achieve with real estate could elude you indefinitely.

-

Becoming complacent with your finances

Failing to take honest stock of your financial position before borrowing to acquire additional housing assets, when rates are at such an all time low, could see all of your investment dreams unravel down the track.

If your budget suggests that you could afford the mortgage repayments, but things may be a little tight financially, or there might be changes to your income on the back of significant life events like starting a family, then perhaps you need to do a little more number crunching.

Ideally, you should still be able to comfortably afford your mortgage at an interest rate of around 7 to 8 per cent, which is still held as the long-term average. And don’t forget to allow for a cashflow buffer in case of emergencies!

-

Thinking anything will do

In tightly held markets when property is moving at a relatively fast pace, it’s easy to assume that you can buy any old house and just wait for the revenue to come rolling in.

Optimal asset selection is critical to building a successful, long-term property portfolio. The investment you select must align with your strategy and goals, and demonstrate a history of sound, long-term growth with promising future prospects.

It must be a proven performer over the number of years you plan to hold it, irrespective of market ups and downs.

-

Not following a game plan

This is the most common downfall of investors who start out in overly optimistic markets. They leap without looking carefully at the elements that matter most – where you are right now, where you hope to be and how you plan to get there in between.

If you’re investing in a property because you can, not because you necessarily should or even have a clue whether it’s right for you, then what exactly is the purpose of the exercise?

If you would like to discuss whether purchasing a property investment at this particular point might suit your investment strategy and current financial position, the Trilogy team can help.

Click here now to connect with us and we can help you to identify and manage the risks, rather than ignoring them at your peril.

About the Author

Since 2008, David Thomas has built a business aimed at servicing the needs of property investors. Now recognised as one of the top 10 independent mortgage brokerages in the country, David and his team have settled almost 2 billion dollars worth of residential and investment loans over the last decade.

Known for his straightforward, accessible style, David believes by educating people about their mortgages; they fare better in the market. By sharing his expertise openly, some of the people he educates will likely become his clients. It's a win-win approach.

David Thomas is a credit representative (Representative Number 506153) of BLSSA Pty Ltd, ACN 117 651 760 (Australian Credit Licence 391237).